Liquefied natural gas will either be a major economic boon for the Canadian economy, or a dud, depending on which recent report you favour.

The Institute for Energy Economics and Financial Analysis (IEEFA) on Monday published a report responding to an earlier economic analysis by the Conference Board of Canada that estimates the annual investment in LNG in Canada could total $11 billion annually between 2020 and 2064 -- $500 billion in total.

B.C. alone would generate 71,000 new jobs per year and more than $4.6 billion in wages, the Conference Board estimated.

“At $2 billion in annual provincial taxes and royalties, the LNG sector could become one of the largest revenue generators in B.C.,” the report stated.

However, that analysis does not indicate how many LNG export projects that calculation is based on. In a report released Monday, the IEEFA points out only one large LNG project is moving forward in Canada – the $40 billion LNG Canada project in B.C. – and casts doubt on whether a second one – Kitimat LNG – will ever be built.

“The most important fact is that the fundamentals of British Columbia’s LNG export cost structure are not competitive enough to keep private capital interested,” the IEEFA report states. “Although many pundits cite political and regulatory issues, Canadian LNG’s biggest problem is profitability.”

The IEEFA suggests Canadian LNG projects won’t be able to compete with Qatar, on a price basis. Then again, few countries can.

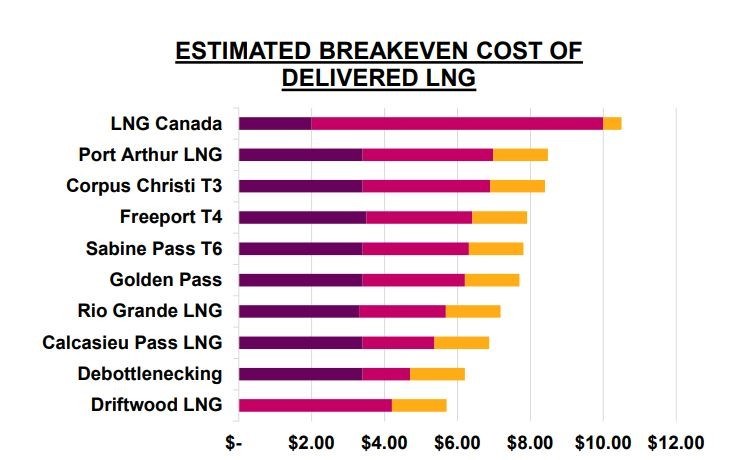

It’s estimated that any new large LNG projects will need a break-even price of US$7 to US$8 per MMBTU of delivered LNG.

Qatar is expanding brownfield projects and restructuring contracts to build new LNG export facilities that could deliver LNG at US$5 MMBTU, Clark Williams-Derry, an analyst with the IEEFA, told BIV News.

“That’s going to put price pressure on the entire global stack of LNG projects,” Williams-Derry said.

“Qatar is attempting to boost LNG exports and capture market share with low prices. This will make it much harder for higher-cost projects to succeed, not just in Canada but likely in the U.S. and Australia as well.”

Asked if Canadian projects face challenges that the U.S. and Australia don't, Williams-Derry pointed to a recent S&P Global Platts analysis that pointed out that the break-even capital costs are much higher in Canada than American LNG proposals.

That’s mainly due to remoteness of location and the need for new pipelines, like Coastal GasLink.

But the same S&P Global Platts analysis also points out that Western Canadian LNG projects have the lowest transporetation and feedgas costs, compared to U.S. projects. Of all the North American proposals, B.C. LNG projects are much closer to Asian ports in shipping distance.

So while the upfront capital costs of building an LNG plant in B.C. is much higher than in the U.S., the ongoing transportation and feed-gas costs are much lower.

“LNG Canada offers large shipping and feedgas savings over US Gulf Coast,” the S&P Global Platts report notes.

“Given a weaker price outlook, LNG Canada is looking less attractive, but will still run at high utilizations once complete.”

The IEEFA report happened to come out shortly after the release of the International Energy Agency (IEA) 2020 World Energy Outlook, which notes that the global pandemic has shocked the oil and gas industry, something which it estimates could take some years to recover from. It notes that natural gas is more resilient than oil, however.

“Natural gas recovers quickly from a drop in demand in 2020,” the outlook predicts. “Demand rebounds by almost 3% in 2021, then rises to 14% above 2019 levels by 2030, with growth concentrated in Asia.”

And while the IEA now expects that it will take longer than expected for LNG demand to outstrip a supply surplus, it expects the demand for both natural gas and LNG to increase over the coming decade, notably in China and India.

“China recovered quickly from the crisis in terms of energy demand, which sees only a 1% decline in 2020 before rising to 13% above 2019 levels by 2030,” the global outlook states. “Driven by strong policy support, renewables account for around nearly half of the growth and natural gas for around one-third.

“Liquefied natural gas is expected to remain the main driver behind global gas trade growth, but it faces the risk of prolonged overcapacity as the build-up in new export capacity from past investment decisions outpaces slower than expected demand growth.”

In other words, the demand for LNG in Asia won’t stop growing, according to the IEA -- it will just take longer for demand to exceed supply. It is worth noting what the IEA has to say about Canada in its country snapshots:

“Canada’s LNG sector is poised to take off, which will bolster Canada’s energy ties with Asia and will help monetize an abundance of western shale gas resources.”