If you live in Vancouver, are under the age of 40 and have your heart set on living in a detached house, you’re more likely than anywhere else in the country to turn to your parents for help.

At least, that’s the best educated guess from observers of the city’s real estate market. Like the controversial issue of foreign ownership, there is no data available on the phenomenon.

“The combination of very, very high house prices means that you have generations, whether it’s parents or the grandparents, who have a whole bunch of house equity,” said Tsur Somerville, a professor at the University of British Columbia’s Sauder School of Business.

“You’ve got kids for whom it is, given the incomes here, difficult to [save].”

In 2012, Vancouver’s median income was $71,140, according to Statistics Canada. Calgary, Edmonton, Toronto and Montreal all had higher median incomes.

Chris Catliff, CEO of BlueShore Financial in North Vancouver, said his credit union has seen an increase in the number of parents who want to use the equity in their homes to help their children buy into a detached-home neighbourhood.

According to Catliff, the trend is linked to an increase in wealthy immigrant buyers who are buying homes as an investment, which has helped push prices up. Meanwhile, homeowners over the age of 55 who purchased homes in the 1970s or ’80s have seen a steep rise in their home equity.

They are now increasingly using that equity to help their children buy a house, Catliff said.

“The desire of parents is often to get their children and grandchildren into [detached-home] neighbourhoods, with great schools, and near them,” he said.

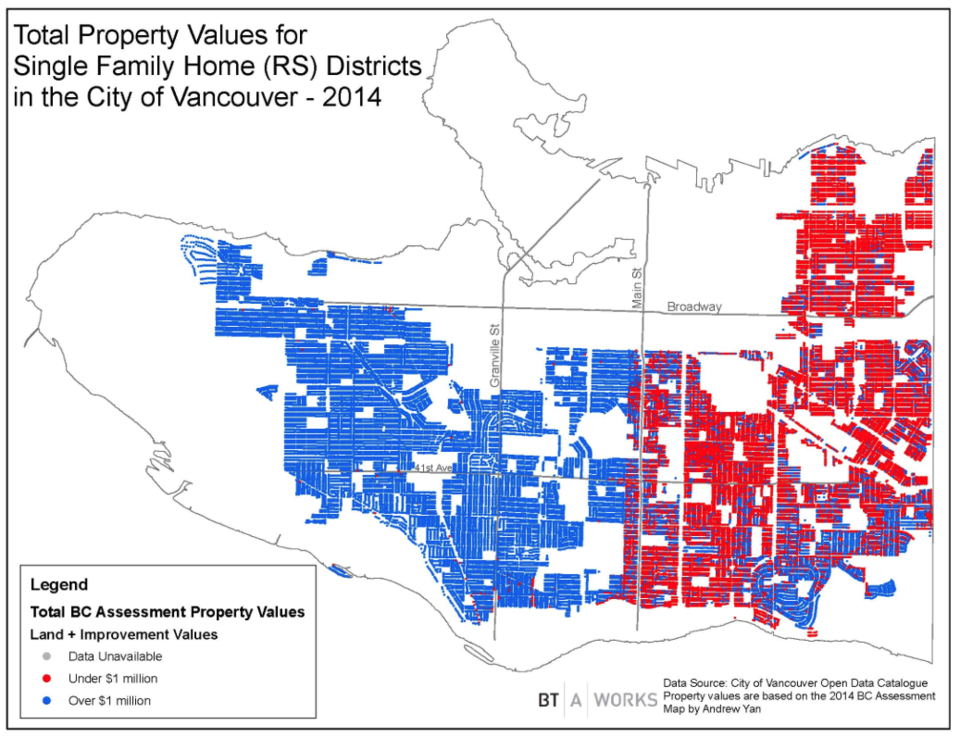

Paul Eviston, a realtor who specializes in East Vancouver, said he has seen more parents helping children buy real estate over the past two years. Houses on the city’s traditionally lower-priced east side are now regularly listed at over $1 million.

“If you think about it now, to get into a reasonable detached home on a full city lot, your price point is about $1.3 million,” Eviston said.

That means the buyer would have to come up with $325,000 just for the down payment.

“If someone’s coming out of a townhouse that’s worth maybe $700,000 and they’re going up $600,000, they’re going to have some of that equity but they’re probably going to need around $100,000 to make the jump.”

That gift from the parent effectively lowers the home price, meaning that a $1 million home would get knocked down to $750,000 if the purchaser got a gift of $250,000 for a down payment from his or her parent.

“As long as the parents are gifting the money, it’s not calculated into their total debt service ratio,” Eviston said.

It's become more common for homes on the city's east side to be priced above $1 million. Source: Bing Thom Architects

Many of the younger couples he sees buying houses worth over $1 million have high dual incomes, in the $300,000 range, and so can afford the hefty monthly mortgage payments.

That’s why RBC’s quarterly affordability index for Vancouver is perennially shocking but doesn’t tell the whole story, said Ryan Berlin, director of Vancouver research firm Urban Futures.

RBC’s housing affordability index for November showed that it would take 83% of gross household income to afford a detached home in Vancouver, compared to 56.3% in Toronto. In a March 3 report, RBC said Vancouver home prices are a drag on the overall housing affordability for the province.

“What we are increasingly inclined to do is not [compare] incomes to price but incomes to payments,” said Berlin. “[Banks] won’t lend to you if you’re spending more than 44% of your gross income each month servicing debt. That includes your mortgage.”

To get more detail on this trend, Urban Futures has ordered custom data from Statistics Canada – but the firm doesn’t expect to receive the data for several months. The Canada Mortgage and Housing Corp. has identified the issue for future study.

“The boomers are the wealthiest generation in history, and they have savings, they have other assets,” Berlin said.

In a 2014 speech to the Urban Development Institue, condo marketer Bob Rennie said wealth transfer between generations is increasing and will help to keep real estate demand in Vancouver strong.

Wealth transfer is part of the equation keeping detached-house prices in Vancouver very high, Somerville said. But there are also many other factors, such as scarcity of detached homes, pressure on the region’s land base and immigration trends.

As for Vancouver residents who make much less than $300,000 and can’t rely on help from their parents? Well, buying a house in Port Coquitlam instead of Vancouver isn’t the worst thing in the world, Somerville said.

“Are we creating a real divide between the haves and the have-nots?” Berlin asked. “Before we answer that question we should have more data.”

@jenstden